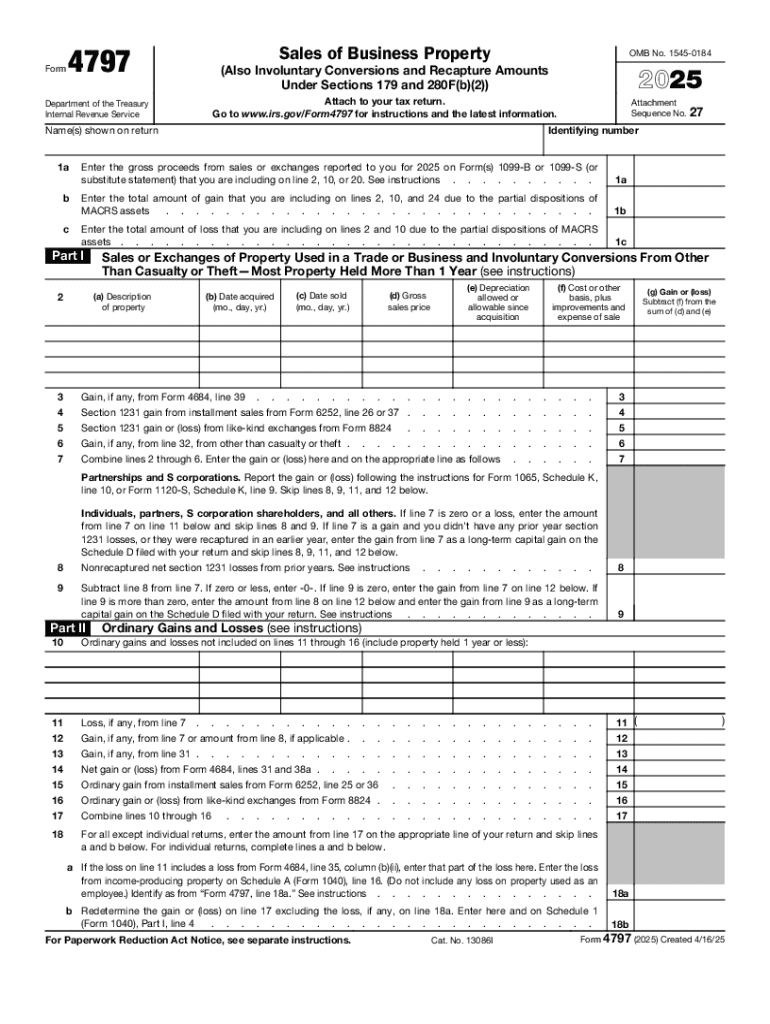

IRS 4797 2025-2026 free printable template

Get, Create, Make, and Sign IRS 4797

Instructions and Help about IRS 4797

How to edit IRS 4797

How to fill out IRS 4797

Latest updates to IRS 4797

All You Need to Know About IRS 4797

What is IRS 4797?

Who needs the form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

Components of the form

What information do you need when you file the form?

FAQ about IRS 4797

What should I do if I discover an error on my submitted IRS 4797?

If you find an error after submitting IRS 4797, you can file an amended version of the form. It’s essential to ensure all corrections are accurate to avoid discrepancies during processing. Follow the IRS guidelines to properly amend your submission, and if necessary, include any relevant documentation to support your corrections.

How can I check if my IRS 4797 has been received and processed by the IRS?

To verify the status of your submitted IRS 4797, you can use the IRS online tools or contact their helpline. If you filed electronically, ensure to save the confirmation details from the e-filing process as it can serve as proof of submission. Be aware of common rejection codes that may affect processing.

What are some common mistakes to avoid when filing IRS 4797?

Common errors when filing IRS 4797 include incorrect asset descriptions and miscalculating gain or loss. To avoid these pitfalls, double-check your entries against supporting documentation and consider consulting with a tax professional if complexities arise. Accurate reporting is crucial to ensure compliance and prevent audits.

Are e-signatures acceptable when filing IRS 4797 electronically?

Yes, e-signatures are acceptable for electronically filed forms like IRS 4797, provided that you follow the specific IRS procedures for electronic submission. Ensure your signing method complies with the standards set by the IRS to maintain legality and protect your data throughout the filing process.